Introduction to Payroll in Nepal

Most businesses in Nepal set up payroll the same way: hire an accountant, build a spreadsheet, pay salaries on the 25th, file taxes when reminded. It works. Until it doesn’t.

A missed SSF deposit triggers a 10% interest penalty. A TDS filing submitted after the 25th of the Nepali month attracts fines. An employee enrolled late in the Social Security Fund puts the employer, not the employee, at legal risk. And with FY 2082/83 tightening compliance requirements across the board, businesses are discovering that what passed quietly before is now surfacing in audits and business registration renewals.

This guide is for founders, HR managers, and finance teams who want to understand how payroll actually works in Nepal, not the generic checklist version, but the specific numbers, deadlines, and regulatory traps that catch growing businesses off guard.

Table of Contents

The Anatomy of a Nepalese Payslip

Before anything else, you need to understand what you’re calculating. A Nepalese employee’s gross pay is typically made up of:

- Basic salary: the foundation everything else is calculated against

- Allowances: housing, transport, medical, and sometimes Dashain bonus (equivalent to one month’s basic salary under the Labour Act, 2017)

- Incentives or performance bonuses: taxable and SSF-applicable depending on structure

From this gross figure, two types of deductions come off before the employee sees a rupee: statutory deductions (SSF, income tax) and any voluntary deductions (CIT, loans). What remains is net take-home pay.

Getting the basic salary figure right matters disproportionately. Most statutory obligations, including SSF contributions and gratuity calculations, are anchored to basic salary, not gross. An employee on NPR 80,000/month gross with NPR 40,000 basic has a very different compliance footprint than one where the split is 60,000/20,000.

Social Security Fund (SSF): What Every Employer Must Know

Nepal’s SSF, established under the Social Security Act, 2018 (2075 BS), is now the single most significant statutory obligation in private sector payroll. It is not optional. The Social Security Act requires every registered company to enroll itself and its employees, regardless of headcount. A company with one employee has the same obligation as one with five hundred.

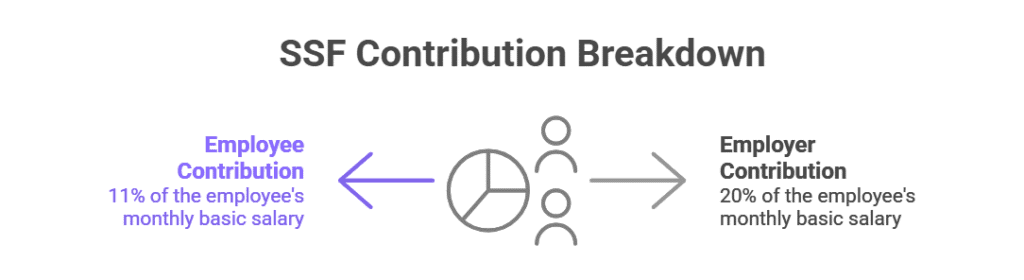

The Contribution Math

The total SSF contribution is 31% of the employee’s monthly basic salary, split as follows:

| Contributor | Rate |

|---|---|

| Employee | 11% of basic salary |

| Employer | 20% of basic salary |

| Total | 31% of basic salary |

This 31% isn’t pooled into a single bucket. It’s allocated across four protection schemes:

- Medical Treatment, Health & Maternity: covers hospitalization, treatment, and safe motherhood for the employee and their spouse

- Accident & Disability: provides compensation for work-related injuries or permanent disability

- Dependent Family: monthly allowance to the spouse (60% of last basic salary) and up to two children (40%, pro-rata) if the contributor dies before retirement

- Old Age / Pension: the bulk of contributions, accumulating for retirement, calculated by dividing (total contributions + investment returns) by 160 to determine a monthly pension

An important practical note: SSF replaces the need for separate provident fund, gratuity, and medical insurance arrangements. If your employees are enrolled and contributions are flowing, you are not legally required to maintain parallel PF or gratuity schemes.

Deadlines and Penalties

- Employers must deposit contributions within 15 days from the end of each Nepali month.

- New employees must be enrolled within 3 months of their hiring date. The employer bears full liability for any failure to enroll.

- Late deposits attract 10% annual interest on the outstanding amount.

- From FY 2082/83, SSF compliance is verified at business registration renewal, and non-compliant businesses can face processing blocks.

How TDS on salary works (FY 2082/83)

- Nepal’s income tax is progressive, governed by the Income Tax Act, 2058, and amended annually via Finance Acts.

- For salaried employees, TDS is deducted monthly, but the basis is annual taxable income: employers:

- Estimate annual taxable‑salary income (after EPF/SSF/CIT, etc.).

- Apply the individual’s marital‑status‑specific slab.

- Divide the total annual tax by 12 to get monthly TDS.

For unmarried individuals (single)

| Annual taxable income (NPR) | Tax rate |

|---|---|

| Up to 5,00,000 | 1% (Social Security Tax / SST) |

| 5,00,001 – 7,00,000 | 10% |

| 7,00,001 – 10,00,000 | 20% |

| 10,00,001 – 20,00,000 | 30% |

| Above 20,00,000 | 36% |

For married individuals (couple assessment)

| Annual taxable income (NPR) | Tax rate |

|---|---|

| Up to 6,00,000 | 1% (SST) |

| 6,00,001 – 8,00,000 | 10% |

| 8,00,001 – 11,00,000 | 20% |

| 11,00,001 – 20,00,000 | 30% |

| Above 20,00,000 | 36% |

Note: Married individuals get a higher SST and first‑10% threshold than single taxpayers, but the top marginal rate remains 36%, not 39% for FY 2082/83.

Social Security Tax (SST) and SSF

- The 1% Social Security Tax slab applies to the first NPR 500,000 (single) / 600,000 (married) of taxable income.

- Crucially:

- If an employee is enrolled in the Social Security Fund (SSF) and SSF contributions are being made, the 1% SST is waived for that employee.

- In practice, for a properly enrolled SSF employee, tax effectively starts at 10% on income above 500,000 (single) or 600,000 (married); the 1% bracket functions as a zero‑rate band.

In payroll practice, this means:

- SSF‑enrolled → 1% SST ignored; use 10% as first applicable rate.

- Non‑SSF → 1% SST applied to first threshold band.

TDS Filing Deadlines

Deducted TDS must be deposited to the IRD within 25 days of the end of the Nepali month in which the deduction was made. Filing is done electronically via the ETDS system. Missing this deadline attracts penalties, as late TDS payment carries both fines and interest under the Income Tax Act.

Annual income tax returns for salaried employees are due by the end of Ashwin (approximately mid-October) each year.

The Compliance Calendar: What Happens When

The single biggest operational risk in payroll is deadline management. Here’s what recurring compliance looks like over the fiscal year:

| Obligation | Frequency | Deadline |

|---|---|---|

| SSF contribution deposit | Monthly | Within 15 days of month-end |

| TDS salary deposit (ETDS) | Monthly | By 25th of following Nepali month |

| SSF new employee enrollment | Per hire | Within 3 months of hiring |

| Annual tax return (employees) | Annual | End of Ashwin (~mid-October) |

| Business registration renewal (SSF compliance check) | Annual | Per company renewal cycle |

For a company paying 20 employees monthly, this means a minimum of two compliance filings every single month. Manual processes like spreadsheets and phone calendar reminders are how most small businesses manage this. And it works until a public holiday shifts the processing window, someone is on leave, or the bank system is down on the 24th.

Where Payroll Processing Actually Breaks Down in Nepal

The problems in most Nepalese business payrolls aren’t mysterious. They fall into a few recurring categories:

Basic salary structuring mistakes. Because SSF contributions are calculated on basic salary, some employers artificially suppress the basic component by paying employees a low basic figure and loading up allowances instead. This is increasingly scrutinised, and the SSF regulations allow the fund to dispute contribution calculations where basic salary appears unreasonably low relative to gross.

Inconsistent TDS recalculation. A common scenario: an employee gets a 15% salary hike in Poush (December/January). The payroll team updates the salary but forgets to recalculate the remaining months’ TDS based on the new annual income projection. The employee ends up under-deducted, creates a tax shortfall, and either the employee or employer faces a reconciliation problem at year-end.

Dashain bonus mis-classification. The Dashain bonus (equivalent to one month’s basic salary, mandated under the Labour Act for permanent employees) is taxable income. Many businesses either don’t include it in annual TDS projections or process it as a separate payment without adjusting the year’s TDS deductions.

Part-time and contract worker exposure. There is a widely held belief that part-time or contract workers fall outside SSF and labour compliance. Under both the Labour Act, 2017 and the Social Security Act, 2018, all categories of formally employed workers, including part-time, contract, and work-based staff, are subject to SSF enrollment. The only meaningful exemptions are independent consultants and certain government security sector employees.

Delayed exit settlements. When an employee leaves, the employer must calculate and settle outstanding entitlements: accrued leave encashment, any remaining Dashain bonus (pro-rated), and the SSF account closure process. Exit payroll is often handled ad-hoc and creates disputes.

Building a Payroll Process That Doesn’t Create Problems

For businesses with up to 50 employees, the core infrastructure is not complicated. What matters is consistency and documentation.

Define salary structure clearly from day one. Every offer letter and employment contract should specify basic salary, allowances, and the split explicitly. Ambiguous salary structures create SSF calculation disputes and make TDS harder to defend in audits.

Maintain a payroll register. A monthly payroll register should document, for each employee: gross pay, all deductions (SSF employee share, TDS, others), net pay, and cumulative figures for the fiscal year. This is your primary audit document.

Reconcile SSF and TDS filings against your payroll register monthly. The amount you deposited to SSF and IRD should tie back exactly to what appears on the payroll register. A five-minute reconciliation each month prevents hours of untangling later.

Build the compliance calendar into your accounting process. The 15th and 25th of each Nepali month are hard deadlines. Buffer your processing cycle so payroll is calculated and approved at least three working days before deposit deadlines.

Document every salary change. Increment letters, bonus calculations, and revised TDS workings should be filed and retained for at least seven years, which is the standard audit window under the Income Tax Act.

The Case for Outsourcing Payroll in Nepal

There is a growing category of businesses in Nepal, especially startups scaling from 10 to 50+ employees, foreign company branch offices, and businesses managing distributed workforces across districts, where in-house payroll management creates disproportionate risk relative to the cost of outsourcing.

The decision to outsource isn’t really about the monthly calculation. It’s about 3 specific pain points that become expensive:

Regulatory change management. Nepal’s Finance Act is updated annually every Ashad (June/July), bringing changes to tax slabs, SSF caps, TDS rates, and compliance requirements. An in-house team managing payroll as a part-time function will often miss these changes or discover them late.

Multi-jurisdiction complexity. Companies with staff across Kathmandu and provincial offices, or businesses employing migrant workers and foreign nationals, face additional layers: different allowances, non-resident tax rules (flat 25% for non-residents), and varying benefit structures.

Audit and penalty exposure. The IRD and the SSF have both intensified enforcement in recent years. A payroll service provider carries liability for the accuracy of their calculations and filings. An in-house team relying on a spreadsheet does not come with the same accountability structure.

A Note on Technology

The Nepalese payroll software market is maturing. The SSF’s own portal (ssf.gov.np) now supports online employer registration, contribution tracking, and an SMS verification system (sending “SSF” to 41042). The IRD’s ETDS system handles TDS filing electronically. Several accounting platforms available in Nepal integrate payroll processing with tax filing workflows.

The tools exist. The barrier to digitising payroll is usually not cost but inertia. Most businesses doing payroll in Excel have been doing it that way for years, and switching requires a one-time effort to migrate historical data and train staff. That one-time investment typically pays for itself within a year in avoided penalties and staff time.

The Bottom Line

Payroll in Nepal has a reputation for being complicated, but most of the complexity is front-loaded. Once a business has its structure right, with salary splits documented, SSF enrollment done, TDS methodology established, and a compliance calendar in place, monthly payroll processing is genuinely routine.

The mistakes that create problems aren’t usually mathematical errors. They’re structural issues: salary architectures that weren’t thought through, enrollment deadlines that slipped, bonuses that weren’t factored into TDS projections. The time to fix those is before an audit or a disgruntled former employee files a complaint with the Department of Labour. Not after.

If you’re setting up payroll for the first time or inheriting a process that hasn’t been reviewed in years, start with the SSF enrollment status of every employee and work backwards from there.

Frontline Consult provides payroll management, SSF compliance, and tax advisory services for businesses in Nepal. If you’d like a compliance review of your current payroll structure, reach out to our team.

253 views